Trinity correction

The Trinity Study is often cited as the foundation of the 4 percent rule, and it is something I personally use as a baseline for my own FIRE planning. At a high level, it answers a simple question: if you retire with a balanced portfolio and withdraw a fixed, inflation-adjusted amount each year, what withdrawal rate historically survived a 30 year retirement? Using historical data, the study found that roughly 4 percent worked about 95 percent of the time.

One question that came up in an investing forum discussion I was following was whether people really retire at random points in the market. In practice, many people retire after strong market runs, when portfolios are at or near all time highs and they have just crossed their number. A lot of the classic Trinity failures look like this: you barely retire, then a correction hits immediately after. This is commonly referred to as sequence risk. But, it got me thinking about the flip side. What if retirement begins during a correction instead? While sequence risk doesn’t go away, it is somewhat mitigated.

This is not about active market timing or trying to predict bottoms. It is a much simpler scenario: if you retire when markets are already down 5 percent, 10 percent, or more, then you should be able to command a higher withdrawal rate. Intuitively, if you only hit your retirement number because stocks are at record highs, your margin of safety feels thinner than if you retire after prices have already pulled back.

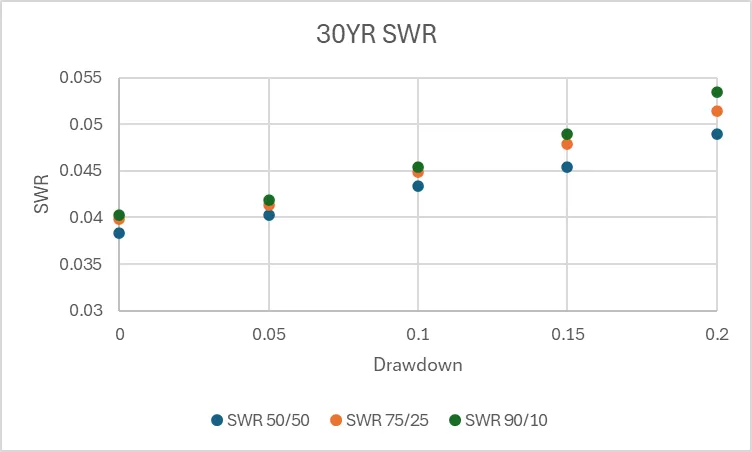

To explore this, I ran a modified Trinity-style analysis using Robert Shiller’s historical data. I used roughly 75 years of data ending in 2025, monthly returns instead of annual, and the same 95 percent success threshold as the original study. A zero percent drawdown case maps very closely to the traditional Trinity setup, and reassuringly, it produces nearly identical results. From there, I filtered starting points to only include months where the market was already in a correction.

The results are pretty fun, if not expected in hindsight. For a 30 year retirement horizon, retiring during a 10 percent drawdown increased the safe withdrawal rate by about 0.5%, depending on asset allocation. Deeper drawdowns pushed that number even higher.

The results are pretty fun, if not expected in hindsight. For a 30 year retirement horizon, retiring during a 10 percent drawdown increased the safe withdrawal rate by about 0.5%, depending on asset allocation. Deeper drawdowns pushed that number even higher.

A concrete example helps. Suppose you have a 2.5 million dollar portfolio and plan to withdraw 100,000 dollars per year at a standard 4% SWR. Based on the historical data, if retirement begins during a moderate correction rather than at a peak, the same risk tolerance supports something closer to a 4.2 percent withdrawal rate. That means either pulling an extra 5,000 dollars per year, or being able to retire with roughly 2.38 million instead of 2.5 million.

That difference can be hard to take advantage of if you are following a rigid savings plan and most of your money is already invested when the correction happens. It becomes much more interesting if you have flexibility, are already close to retiring, or are bringing in outside capital like a business sale, bonus, or inheritance.

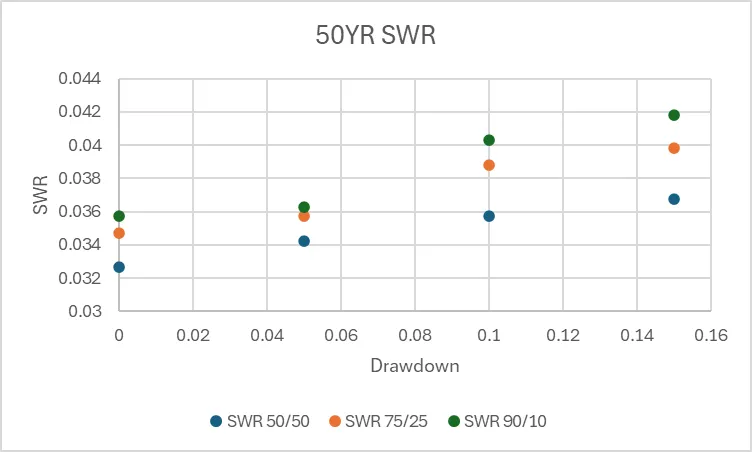

The effect is smaller for very long retirements like 50 year FIRE scenarios. Over that kind of time horizon, a 5 or 10 percent correction matters less. I also did not heavily optimize the 50 year case due to sample size and historical data fidelity issues, though it would be straightforward to expand that analysis with looser constraints.

Conceptually, this lines up well with the logic behind flexible withdrawal strategies. The idea there is that adjusting spending based on market conditions reduces sequence of returns risk. Starting retirement during a drawdown accomplishes something similar. You are beginning withdrawals after some of the downside has already occurred.

I would not recommend delaying retirement or trying to time the market just to catch a correction. That is neither practical nor reliable. But if you find yourself able to retire during a correction, the data suggests you can safely withdraw more than the standard rule of thumb implies. At a minimum, it is a useful reframing. Market conditions at retirement matter, and the 4 percent rule works best as a baseline, not a fixed law.